Small biz owners and sole traders, you can use a balance sheet to make sure your business finances are healthy, hearty, and most importantly, accurate.

If you’ve come across these scary-sounding documents before, you know they’re notoriously difficult to decipher. Or maybe you find them easy to decrypt, in which case, give us a call 👀

All jokes aside, we’re here to help you understand balance sheets, without all the complicated jargon.

A balance sheet shows how much money your business is worth (net worth) based on its assets, liabilities and equity. The main use is to make sure that your books are – you guessed it – balanced. Another is for people like investors, stakeholders and outside regulators to be able to see the health of a business in the current period, a previous one or even how it might perform in the immediate future.

Here’s what information is on a balance sheet:

The basic equation is:

Assets – Liabilities = (owner/shareholder’s) Equity

There are two types of assets and liabilities:

1. The first one is current assets or current liabilities.

2. The second type is non-current assets or non-current liabilities.

Alternatively, you can also refer to them as short-term (current) or long-term (non-current).

Here are some examples:

Equity is the value of what’s left over after you deduct what the company owes (liabilities) from what it owns (assets). That amount is what would go to the owner or shareholders. It essentially represents a shareholder’s or owner’s stake in the company.

As we mentioned, equity = assets – liabilities.

Equity can either be negative, meaning the liabilities outweigh the assets, or it can be positive meaning that there are enough assets to cover the liabilities.

To make your own balance sheet, you need to know a few things about the finances of your company. Oh, and also some maths, so we recommend keeping a calculator handy. Or, if you’re really tech-savvy, you can use a spreadsheet to do the calculations for you 👩💻

You’ll need to know the total amount of current/non-current assets and liabilities that the company has.

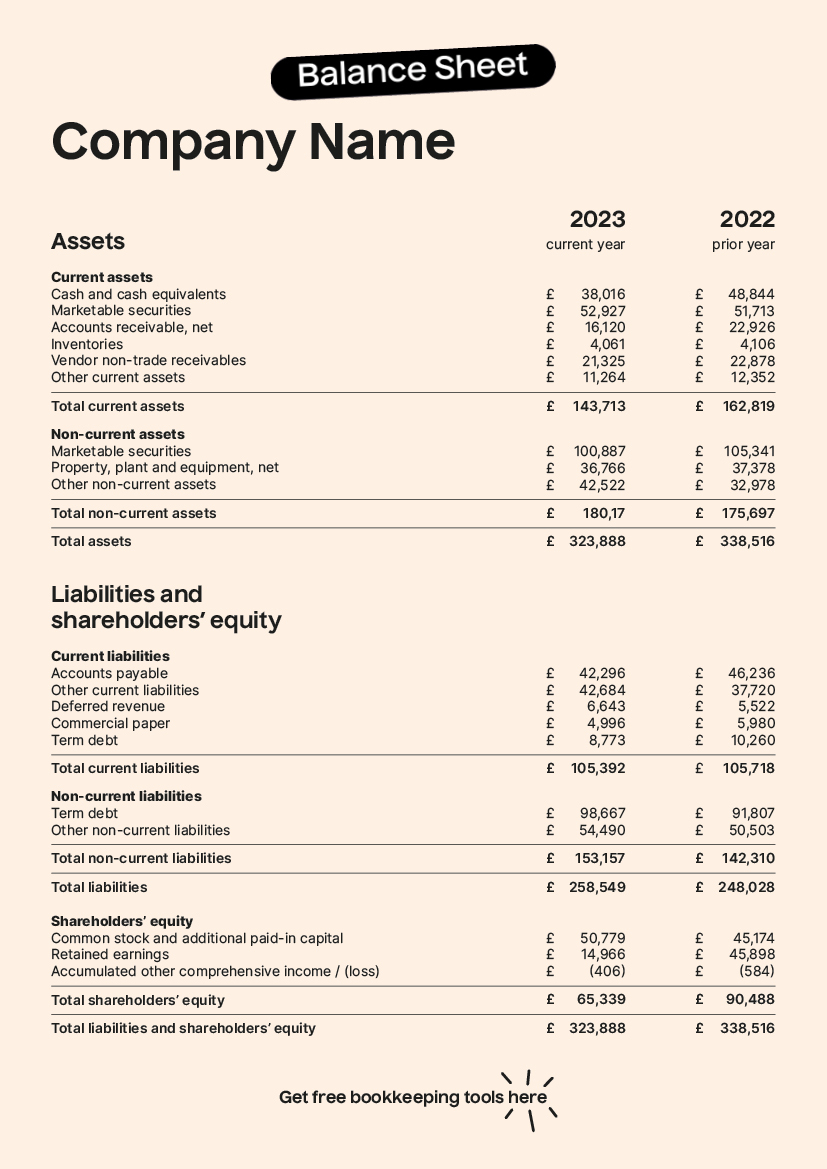

Once you’ve got that data, you can start maths-ing and forming your balance sheet for the current accounting period. Here’s an example of what a balance sheet looks like.

Or just use our template and fill it in to suit you and your business. HMRC also has a template you can follow on their website.

Remember, the goal is to make sure everything balances out at the end. What you own should pay off what you owe and leave you with the leftover equity.

Yep, it should always, always balance.

If it doesn’t, then there could be another explanation. Here are a few reasons for an unbalanced sheet:

It’s when you compare a company’s balance sheet to the general ledger (assets, liabilities, equity, income, expense, gain, and loss transactions of a business) to verify the accuracy of the balance sheet. So, what happens if your balance sheet doesn’t balance? Balance sheet reconciliation.

Translation: Every transaction within the business needs to fall under the asset or liability category and they should all balance to the correct amount of equity.

Once you confirm everything matches, you can be extraordinarily relieved to know that your books are balanced!

That’s one less thing to worry about🙌

If you’re looking for an easier way to keep things in order, our free bookkeeping tools have got you covered in that department.

Create and send invoices, pull your spending straight from your bank account, and track your incomes and expenses from your accounting dashboard. All in one place.

Plus, you can choose to get extra support from an accredited accountant, if you need it!

Manage your self-employed finances in one place with 10/10 bookkeeping tools.

Or see our Guides, Calculators or Taxopedia