Fast, effortless and 100% online. Learn more

One of the major tax implications for high earners is that you start losing your Personal Allowance over £100K— and the dreaded (but unofficial) 60% tax rate. As soon as you start earning over £100,000, you gradually lose your £12,570 income tax Personal Allowance, pound by pound.

Also important to remember is that you may have to do a tax return. HMRC will check what’s known as your Adjusted net income when you do this, to work out whether you owe money or are due a refund based on your high-earner salary.

From April 2023, the threshold for submitting a self assessment increased to £150,000 per tax year. And from April 2024, the threshold was abolished, meaning high earners no longer need to file a tax return.

But, if you’re earning £100k+, you should still make sure to contact HMRC to check you’re on the correct tax code!

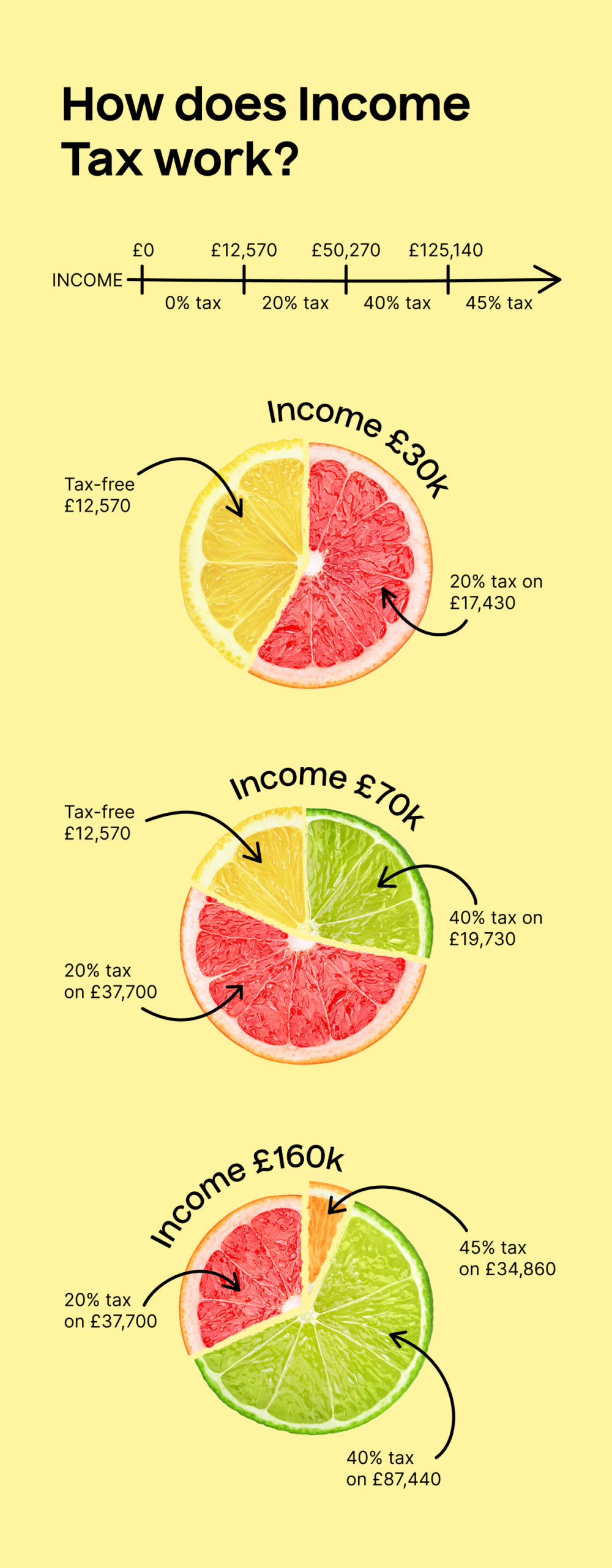

To understand the 60% tax rate, you should first understand the way that income is taxed in general in the UK.

Income Tax is currently charged at the following rates, although this is subject to change depending on the Chancellor’s vision at the time of each Autumn Budget.

The income tax rates in the 2025/26 tax year 👇

| Income | Tax rate | Tax band |

| Up to £12,570 | 0% | Personal allowance |

| £12,571 to £50,270 | 20% | Basic rate |

| £50,271 to £125,140 | 40% | Higher rate |

| over £125,141 | 45% | Additional rate |

You’ll notice in the above table that the 60% tax isn’t mentioned. That’s because it isn’t an official tax band recognised by HMRC. It’s instead a calculation of how much you end up paying when your Personal Allowance is deducted. By losing the allowance, it adds an extra 20% of tax (the basic rate) onto the income you earn between £100,000 and £125,140.

For every £2 that you earn over £100,000, you lose £1 of your Personal Allowance. You also won’t be eligible for additional rate tax until you earn a higher income over £125,141.

It’s confusing. We know.

Put simply, here’s an example:

Now, if you’re a visual learner, we’ve obviously got you. This image will help break down Income Tax and what it means for higher salaries.

Whatever tax you’re liable to pay, you will have to pay by law. That said, there are ways to be more tax efficient.

Here’s a selection of things that you can do to improve your tax efficiency, avoiding the 60% tax trap:

For more information, take a look at this article about ways that you can be tax efficient when you earn over £100,000.

Filing with TaxScouts is just easier. Not only that, but we’re friendlier, jargon-free and have expert accountants on our side.

Or see our Guides, Calculators or Taxopedia