Fast, effortless and 100% online. Learn more

You’ve just been promoted, you’ve got a big commission from your sales. Maybe you got a bonus as a reward for your hard work? Or simply, you’re just earning over £100,000 because you work 100 hours a week.

It should be a reason to celebrate – if only you weren’t paying a higher tax rate than anyone in the UK (even than people earning more than you).

Basically, everyone in the UK is entitled to an amount of money that’s tax-free. This is called the Personal Tax Allowance and it’s worth £12,570 this tax year. Over this, you pay tax in tranches, from 20% to 45% on your income, otherwise known as your taxable income.

Where does the 60% come from? Well, once you earn over £100,000, you start losing your tax-free Personal Allowance – one pound of allowance per every two pounds over this £100,000 threshold.

If you do the maths, this is an income tax rate of exactly 60% for the income between £100,000 and £125,140. And this doesn’t include National Insurance.

This is the second highest tax rate in all of Europe. There is only one other place that has higher tax: Munkedal, a small region in Sweden with a population of 10,000, which has a staggering marginal tax rate of 70%.

The good news is that there are quite a few things you can do to reduce your tax rate.

Here is our advice:

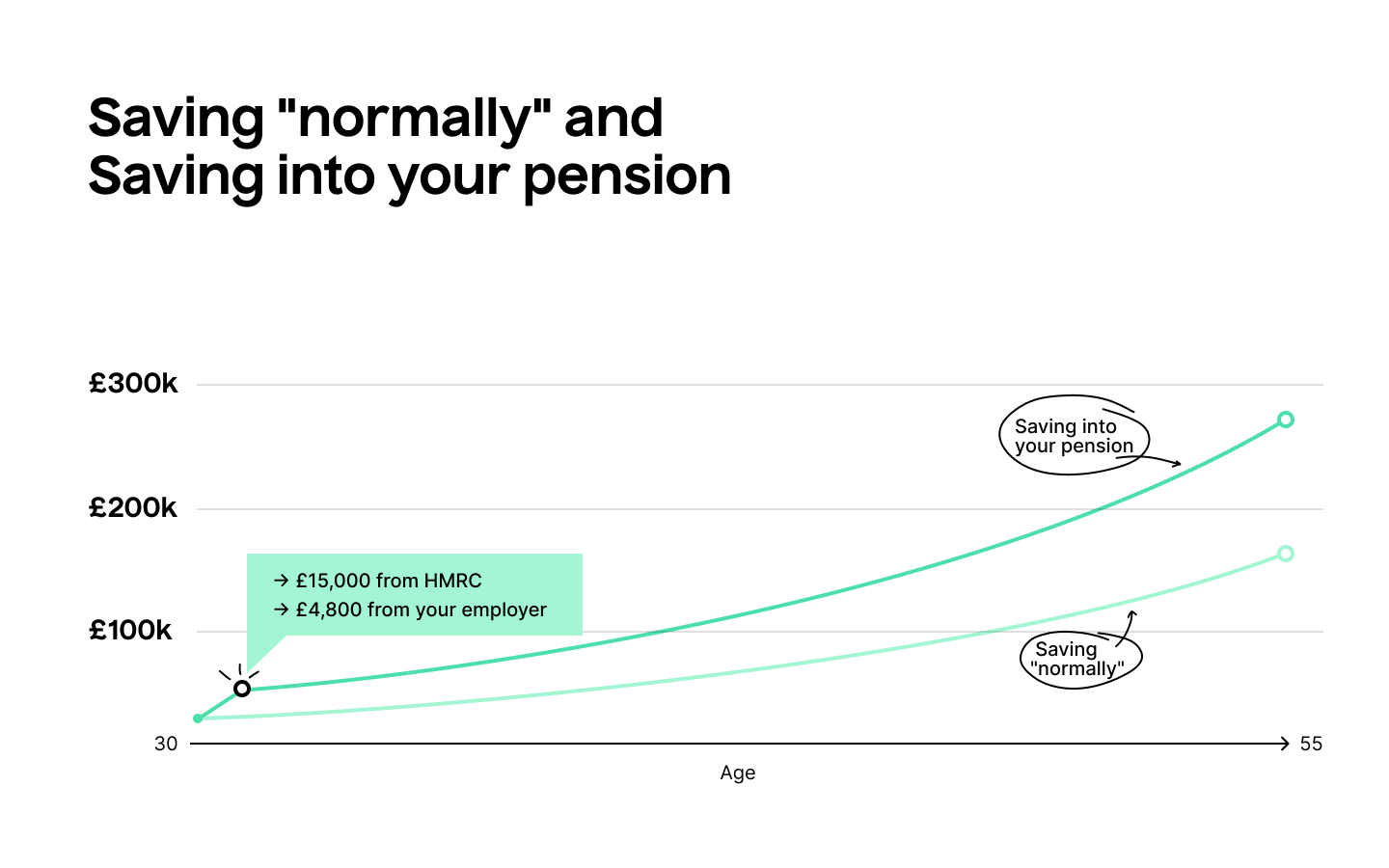

Sure – saving money for retirement is the last thing on your mind when you’re in your 20s or even 30s. It does sound like a bad deal: locking money until you’re 55. In reality, it’s one of the best ways to cut your tax bill.

Three reasons:

Is your employer using “net pay” for your pension contribution?

Good news: whatever you save already includes any tax you would have paid. No need to do anything.

Bad news: it’s quite hard to change how much you save whenever you want to save more – you have to ask your employer whenever you want to save more or less…

Is your employer using “relief at source”? Then how much tax you can get back depends on how much you earn:

Yes!

Look at the example below – for £120,000 your overall tax rate is 32%. With National Insurance it climbs to almost 39% (as per 23/24 tax year rates).

If you save £30,000 into your pension, you’re getting back half of your tax back – and your overall tax rate becomes just under 20%.

| Without private pension | With private pension |

|---|---|

| You earn: £120,000 | You earn: £120,000 |

| You save: £0 | You save: £30,000 |

| Tax relief: £0 | Tax relief: £15,000 |

| Tax you pay: £39,500 | Tax you pay: £23,500 |

| Overall tax rate: 32% | Overall tax rate: 19.6% |

Another way to look at it: compared to saving £30,000 in a normal savings account, by saving it into your pension you get an instant 66% return:

Add a conservative 7% annual return from FTSE100 over the past 30 years, and by the time you’re 55 your £30,000 will be worth a little over £270,000.

That’s a 442% return over 25 years (presuming you save this amount when you’re 30).

This works great if you’re starting out in investment banking or consulting, where usually it’s the bonus that sends you into the 60% tax trap.

By reducing your cash earnings by just a bit, you can push your income below £100,000 – while also getting your bonus.

For example:

All of these are tax-free if you get them through a “salary sacrifice” scheme.

This is another great way to save on tax. Although be aware that startups are risky investments and your capital is at risk. The money you invest could go up or down.

This type of investment works similarly to the pension tax relief: you invest in a startup today and you can get the tax back on that amount through a Self Assessment tax return.

There are three startup investment schemes in the UK:

Plus, if the startup that you invest in makes it big, you don’t have to pay any tax on this profit, either.

How to find startups to invest in if you’re not a professional angel investor:

Just remember to file a Self Assessment and declare these investments: if you don’t, not only will you not get your tax back, the gains from the eventual profit (IPO, acquisition…) will not be tax-free either.

We can help. We offer one-off, personal tax advice from an accredited accountant, especially for high-earners. Whether you’re looking to be more tax-efficient, getting your head around adjusted net income or anything else, we’ve got your back. Just £139 per consultation. Learn more here.

Sign up for important updates, deadline reminders and basic tax hacks sent straight to your inbox.

"*" indicates required fields

Or see our Guides, Calculators or Taxopedia