Fast, effortless and 100% online. Learn more

The additional rate tax is the top rate of Income Tax in the UK. You pay this when you earn more than £125,140 per year.

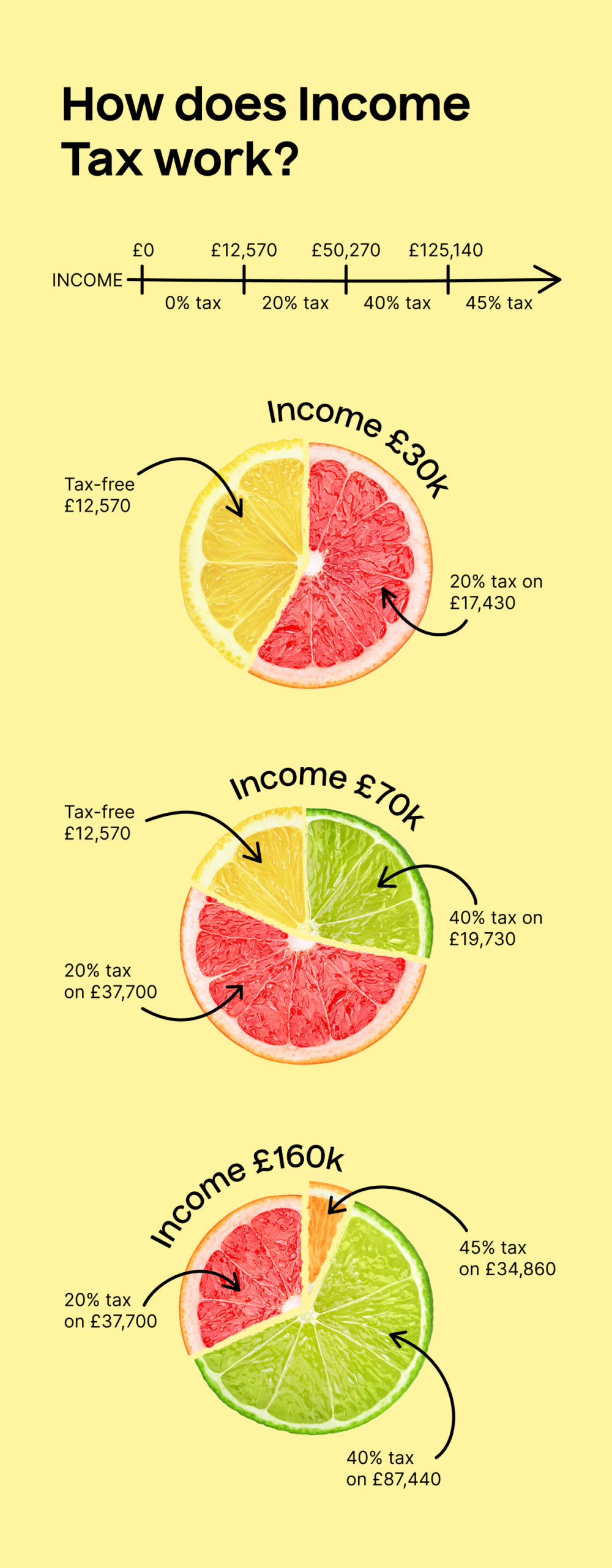

Income Tax is paid by everyone in the UK who earns more than £12,570 per year. The first £12,570 is Income Tax-free and known as the Personal Allowance. However, when you earn more than £100,000 per year, you gradually lose your eligibility for this allowance, £1 at a time.

Take a look at the Income Tax rates for the 2024/25 tax year:

| Income | Tax rate | |

| Up to £12,570 | 0% | Personal allowance |

| £12,571 to £50,270 | 20% | Basic rate |

| £50,271 to £125,140 | 40% | Higher rate |

| Over £125,0140 | 45% | Additional rate |

In the 2024/2025 tax year, the additional rate is 45% on earnings above £125,140. So if your annual income is £170,000, for example, you’re an additional rate taxpayer. This means that you pay 45% tax on your income above £125,140.

In this case, that’s broken down like this:

If you’re in Scotland, the additional rate tax is actually 47% on earnings above the same £125,140 limit.

When you earn more than £100,000, you start to lose your entitlement to the Personal Allowance. You lose it by £1 for every £2 that you earn over £100k. However, you’re not taxed at 45% until you earn over £125,140 which means that between £100,000 and £125,140, you’re taxed an extra 20% on the Personal Allowance that you’re losing. This can be confusing to get your head around, so take a look at our guide on the tax implications of earning over 100k.

Sign up for important updates, deadline reminders and basic tax hacks sent straight to your inbox.

"*" indicates required fields

Or see our Guides, Calculators or Taxopedia