Fast, effortless and 100% online. Learn more

If you make a profit from trading Bitcoin, Litecoin, Ethereum, or any other cryptocurrency, then you might want to know if you can cash out crypto tax-free. Crypto trading is becoming more and more popular, especially with younger traders who are keen to start their first investment portfolios.

However, although these crypto assets have the potential to make you lots of money, it doesn’t mean that they’re not subject to tax. HMRC might not deem crypto to be actual money, but they still see it as a type of personal investment. Like property or shares, any profits you make from buying or selling crypto is taxable.

Crypto, or cryptocurrency, is a form of digital asset that can be used online for the exchange of goods and services.

There are more than 6,700 different cryptocurrencies that are being traded publicly. Some of the most popular types of crypto include:

Because of these reasons, the value and potential of crypto is increasing. As a result, more and more traders are looking to invest in crypto to make profits and increase their investment portfolios.

At different points in its thirteen year history, crypto has fluctuated in value. For example, anyone who bought Bitcoin in 2008 when it was worth fractions of a pound could potentially have made hundreds of millions of pounds in profit in 2021 when its value hit around £40,000.

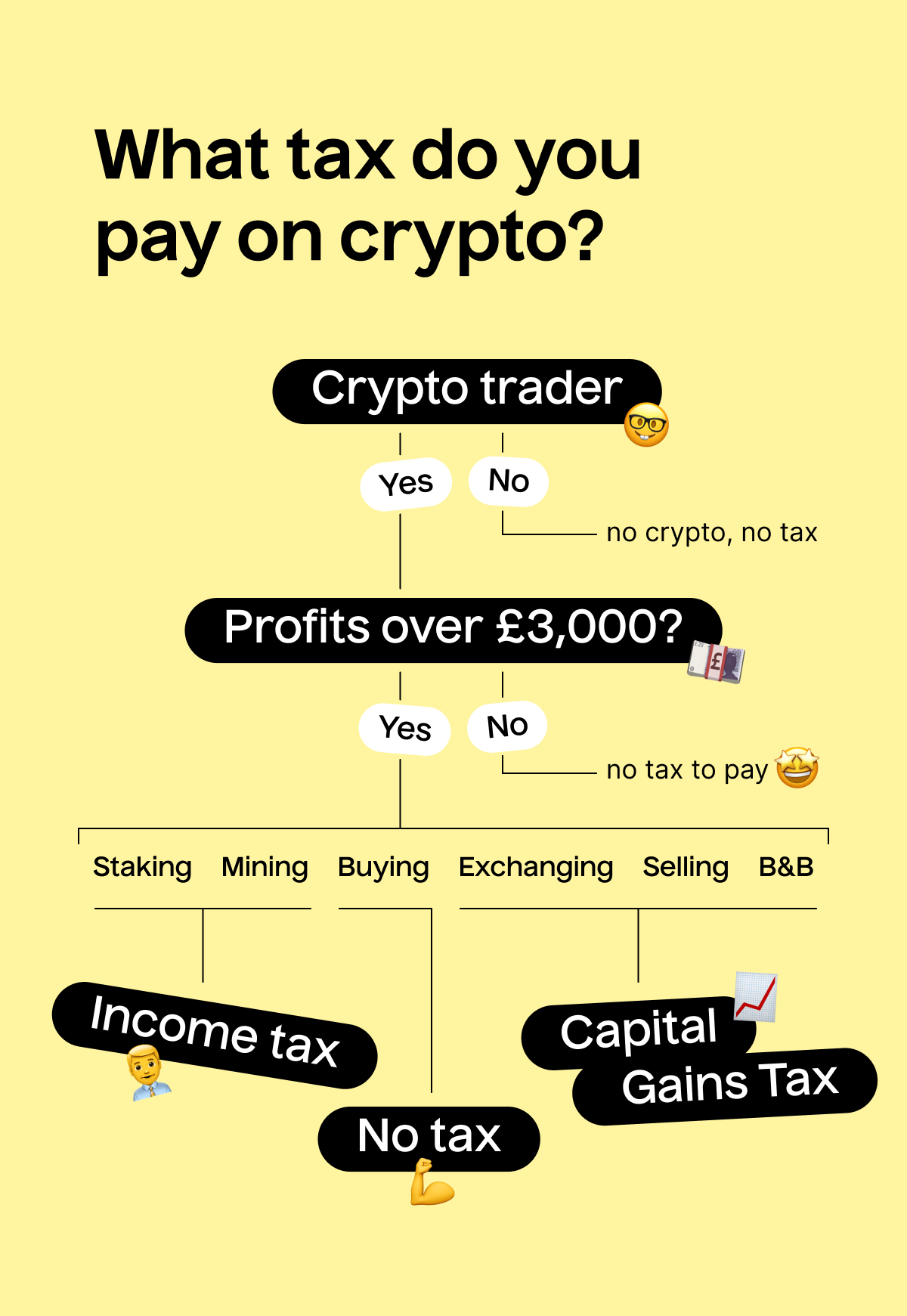

Crypto trading has a reputation of being like gambling, but unlike gambling, you’ll most likely be liable to pay tax on your profits.

If you hold crypto as a personal investment, you’re liable to pay Capital Gains Tax on any profit you make from them. You’ll only pay CGT on the profit above your Capital Gains Tax allowance, which is £3,000 for the 2024/25 tax year. It was previously £6,000 in the 2023/24 tax year. Plus, you could be subject to other taxes depending on your situation.

If your crypto profits exceed the Capital Gains Tax allowance, you’ll have to pay tax at the following rates:

The total capital gains tax (CGT) you owe depends on two things:

Your overall earnings determine how much of your capital gains are taxed at – 10% or 20%.

Our capital gains tax rates guide explains this in more detail.

In your case where your capital gains from shares were £20,000 and your total annual earnings were £69,000:

You pay no CGT on the first £3,000 that you make

You pay £127 at 10% tax rate for the next £1,270 of your capital gains

You pay £3,146 at 20% tax rate on the remaining £15,730 of your capital gains

You need to save

to pay your £3,273.00 tax bill by 31/1/2026 which is in 666 days

You might be surprised to know that the penalties for not declaring your crypto profits can be very severe!

The UK was actually one of the first countries to introduce tax on crypto assets. HMRC is very active in tracking down cryptocurrency tax avoiders, and they’ve even started working with crypto platforms to do this. Coinbase recently handed over information on UK customers who made more than £5000 worth of cryptocurrency between 2017 and 2019 to HMRC.

It’s important to understand that HMRC will not stop its pursuit in finding crypto tax avoiders, so it’s best to be proactive and report and pay your tax in time to avoid any late penalties and further prosecution.

Well, listen up. We teamed up with Koinly to bring you a quick and easy solution: a tool to create crypto tax reports. Want to get your crypto tax report generated and tax return filed all in one? Look no further. Up to 1000 transactions totally free!

Sign up for important updates, deadline reminders and basic tax hacks sent straight to your inbox.

"*" indicates required fields

Or see our Guides, Calculators or Taxopedia