Fast, effortless and 100% online. Learn more

Being self-employed means that you work for yourself rather than an employer.

We know that the accounting side of being self-employed isn’t always straight forward, which is why we’re breaking it down for you!

You can thank us later. 😜

Here’s some simple steps of what you’ll need to do when self-employed:

First, you’ll want to register as a sole trader. You may be wondering, ‘how do I do this?’

Luckily for you, we’ve written a step-by-step guide to registering as self-employed. Check this out here.

But that’s not all, we’ve also answered all the most common questions related to setting up as a sole trader – you can check this out here if needed.

FYI: If you decide you no longer want to work for yourself, you’ll need to let HMRC know so that they aren’t expecting you to file a tax return.

When you register as self-employed, you are given the option between cash basis and traditional accounting.

Choose whichever method works for your business. Cash basis is generally the easiest option as you simply track what goes in and out of your bank account.

Traditional accounting may work for bigger businesses.

Get into the habit of separating your personal and business finances as soon as possible.

This will help you keep better track of your business income and expenditure.

You don’t need to show documents when you file your tax return, but HMRC will ask for them if they ever audit you. For this reason, you should keep all documents and receipts organised.

Keep records for at least 5 years.

Not everyone is required to register for VAT, but you’ll have to register if:

The value added tax (VAT) rates in the 2025/26 tax year 👇

| Tax rate | What the rate applies to | |

| Standard rate | 20% | Most goods and services |

| Reduced rate | 5% | Goods and services like children’s car seats and home energy |

| Zero rate | 0% | Goods and services like most food, books and children’s clothes |

*Businesses earning more than £90,000 in a tax year must register for VAT. See here for more

The tax year is a point of confusion for many. Unlike the calendar year, the tax year runs from April to April. If you’re a LTD company, your business “year” can take place during any 12 month period of your choosing, meaning your filing deadline is unique to you and your business.

As a sole trader, things are a little simpler. Take a look at the below table for the important dates and deadlines to get in your diary for the current tax year.

Key dates in the current 2025/26 tax year 👇

| Deadline | Date | Year |

| Tax year starts | 6th April | 2025 |

| Tax year ends | 5th April | 2026 |

| Register for self assessment | 5th October | 2026 |

| Pay tax bill by PAYE salary | 30th December | 2026 |

| Self assessment deadline | 31st January | 2027 |

🚨 Don’t forget to claim:

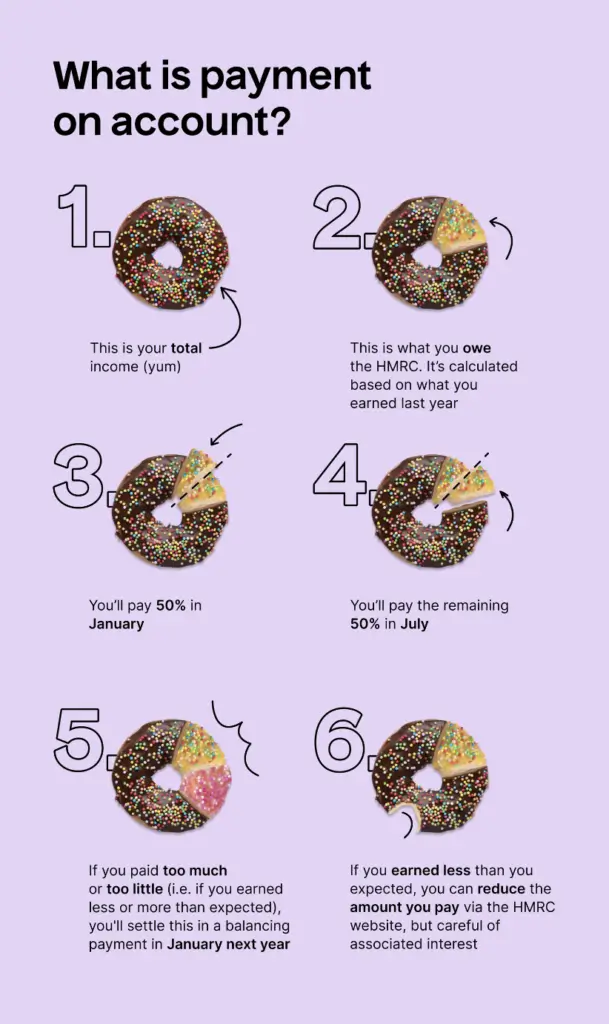

Payment on Account means you pay your annual tax bill in two instalments. You may have to pay up to 150% the first time, but you can read more about Payments on Account here.

To make it a bit more digestible, here’s a visual:

Manage your self-employed finances in one place with 10/10 bookkeeping tools. And all for free – forever and always.

Or see our Guides, Calculators or Taxopedia