Fast, effortless and 100% online. Learn more

In 2021, Bitcoin has continued to surge in value. At the time of writing, 1BTC is worth over £46,000. As a result, many first-time investors have made big profits from investing since its creation in 2008. Wherever you stand on what we can expect to see from the asset over the next year, what is for sure is that if you’ve made a killing and you’re looking to sell, you may owe tax on what you’ve made.

First things first, what is Bitcoin?

It’s a cryptocurrency; a digital asset. In simple terms it’s an online currency that doesn’t have a physical equivalent. It’s not backed by an asset like gold or a traditional currency like pounds or dollars. And when it was created in 2008, 1BTC was worth a fraction of a penny. It’s rollercoastered since then, which is why so many people have made money from it now.

Bitcoin transactions are recorded on a piece of technology called a blockchain. Blockchains are run democratically, unlike a bank like HSBC or Natwest which are run by a centralised power. Because of this, anyone can verify a transaction on the Bitcoin blockchain with the correct technology. The process is called mining, but it can be a bit complicated to get your head around so if you want to read more, take a look at our crypto mining guide.

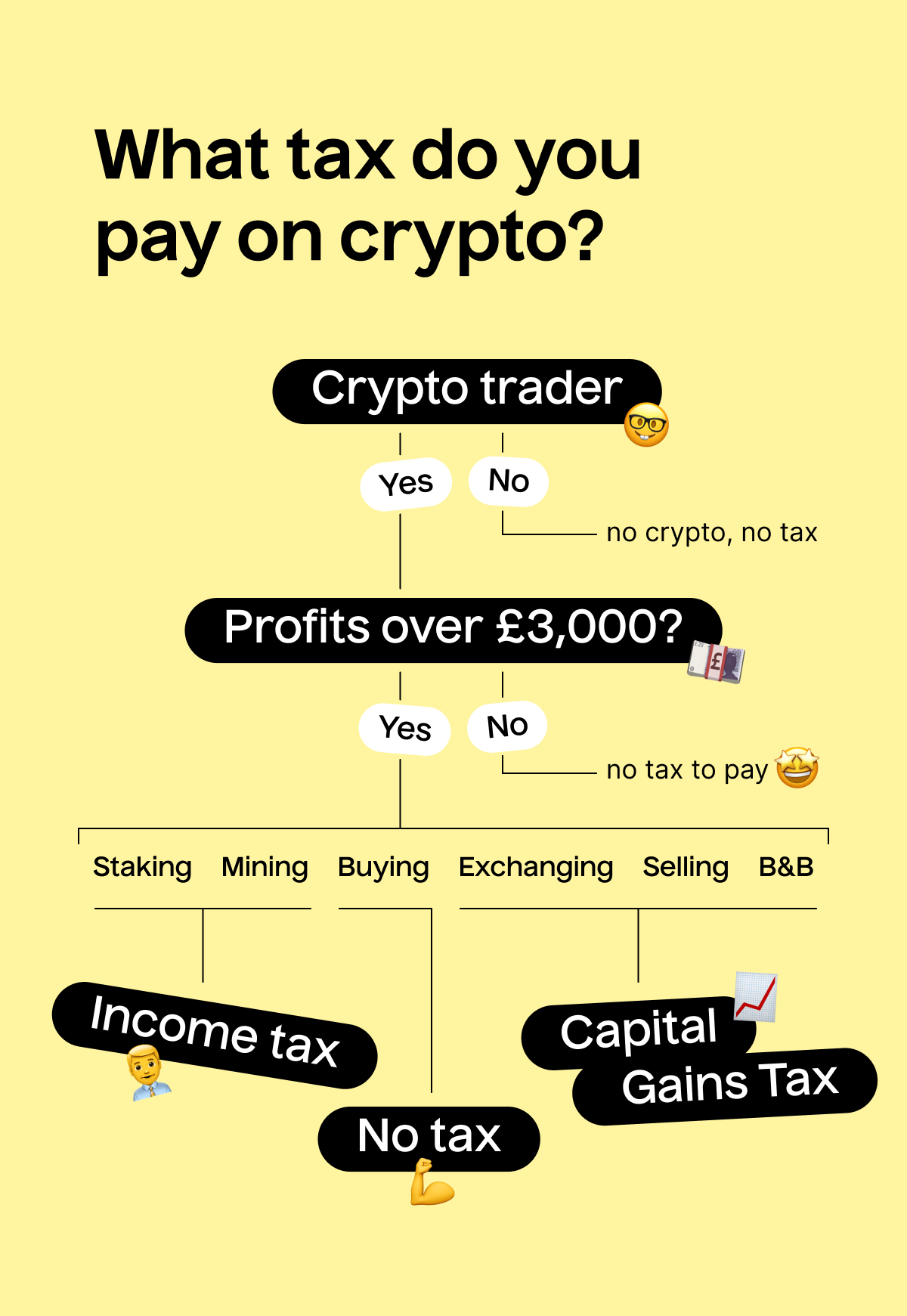

Yes, you may well have to pay tax on your crypto investment earnings. What tax you pay depends on how much you make, when you make it and how you go about investing i.e. is it a side gig or your main source of income?

If you’re trying to avoid any kind of tax, it’s safe to assume that it’s probably at best not advised and at worst not legal! Crypto profits are no different. If you earned enough from trading to be taxed, it won’t be possible to avoid paying out. However you’ll only owe money when you sell (or exchange for profit) your cryptocurrency but not when you buy it or hold (or even HODL 😉) it.

When you hold your Bitcoin in a cryptocurrency wallet, you won’t be taxed on it. This is because HMRC don’t view it as a currency or as money. But if you exchange your crypto (either for another cryptocurrency or into a traditional currency) for a profit, you may be liable to pay tax on these gains. When we say traditional currency, this means Pounds (£), Dollars ($), Euros (€) etc.

There are two types of tax to be aware of. The main one to worry about as a Bitcoin investor (which is how HMRC will view your activities) is Capital Gains Tax (CGT). The other is Income Tax but you’ll only be charged this if your crypto profits make up your full-time income.

CGT is the tax that you pay on your profits. You pay it when you make money from selling a house, from trading shares, and more. In the 2023/24 tax year, you can earn up to £3,000 from profits in Bitcoin before you’re taxed. This threshold is the Capital Gains Tax allowance. Anything you earn in profit above this will be taxed at the following rates:

| Type of asset | Basic rate | Higher rate |

| Shares | 10% | 20% |

| Residential property | 18% | 24% |

| Bitcoin/cryptocurrency | 10% | 20% |

| Other | 10% | 20% |

Looking at the above table ☝️ these are the rates at which you’re taxed on your profits above the £3,000 tax-free threshold.

In the 2024/25 tax year, you pay at the basic rate if your overall income (including your salaried job, any money you earned from side gigs and your crypto profits) is less than £50,270. If your income is £50,271 or more, you’ll be charged the higher rate.

No.

You’ll only owe tax on your gains that you convert to traditional currency (e.g. Pounds, Dollars, Euros etc.).

If you make a capital loss (you sell your crypto for less than you bought it), you can offset this against the gains. But if you do this, you will need to report the loss to HMRC. This can be done on your tax return. You can claim your losses up to 4 years from the end of the tax year that they occurred in.

The tax year, in case you’re not sure, runs from 6th April one year to 5th April the following year. The 2024/25 tax year ran from 6th April 2024 to 5th April 2025. Read more about it here.

No. HMRC don’t see cryptocurrency as currency so there’s not a tax-efficient way to hold it. And this includes being able to hold it in an ISA or other savings accounts. Here’s why you can’t:

Tax-free savings accounts like ISAs let you leave money to sit and mature via interest and they often have a maximum threshold that you can pay in every tax year. By nature, Bitcoin is not a stable asset so its value increases and dips all the time. This is in part because there is a finite supply of bitcoins in existence: there have always been (and will always be) only 21 million bitcoins available. There’s therefore no central organisation (e.g. a government) to manage the flow in the same way that inflation is managed with traditional currencies. If you were to hold Bitcoin in a savings account, you could stand to make a lot of money from savings interest one day that then disappears the next day.

And if it’s not a currency, it can’t be taxed and interest can’t be made from it.

You owe tax based on the point at which you sell your Bitcoin. HMRC describes this as your “disposal” of your crypto assets.

They define this as:

From this point, you should work out what tax year you’re in. If your profits are above £3,000, you will have to declare this to HMRC and pay tax by 31st January. For instance, if you sell your crypto in May 2024, you owe tax for your earnings in the 2024/25 tax year. You pay this tax bill by 31st January 2026.

If you mine crypto, you’ll be taxed in the same way that you might be on any other side hustle. So you’ll be subject to Income Tax. To work out what you’ll owe, just add up all your income to work out what tax bracket you’re in. You can also use our handy employed and self-employed calculator:

As an employee, your employer calculates and deducts Income Tax and National Insurance contributions for you.

But because you’ve earned over £1,000 from self-employment, you need to submit a Self Assessment tax return to pay Income Tax and National Insurance on your earnings.

These are all deducted from your salary by your employer every month.

You pay no Income Tax on the first £12,570 that you make.

You pay £5,486 (20%) on your salary between £12,570 and £40,000.

You pay no NI contributions on the first £12,570 that you make.

You pay£2,194 (8%) on your salary between £12,570 and £27,430

That’s not all. Your employer is also required to pay separate NI contributions, but these won’t come out of your wages. In your case they would need to pay an extra £3,785 – you should see these on your payslip.

You will need to submit a Self Assessment tax return and pay these taxes and contributions yourself. The deadline is January 31st of the following year.

You pay £2,054 (20%) on your self-employment income between £0 and £10,270.

You pay £7,092 (40%) on your self-employment income between £10,270 and £28,000.

You will also have to pay £616 (6%) on £10,270 of your self-employment income.

You will have to pay an additional £355 (2%) on another £17,730 of your self-employment income.

You need to save

to pay your £10,116.80 tax bill by 31/1/2026 which is in 666 days

As a general rule, you can earn up to £1,000 tax-free income outside your salaried job in a tax year. Anything over that and you’ll need to file a tax return.

You’ll only pay Income Tax from Bitcoin profits if crypto trading is your full-time job and it accounts for the majority of your earnings. At that point, you’ll register as self-employed and you will have to pay tax on your earnings over £1,000.

This does also mean that you’ll be able to deduct your expenses, such as mining rigs. This means that you’ll only pay tax on your profits.

Well, listen up. We teamed up with Koinly to bring you a quick and easy solution: a tool to create crypto tax reports. Want to get your crypto tax report generated and tax return filed all in one? Look no further. Up to 1000 transactions totally free!

Sign up for important updates, deadline reminders and basic tax hacks sent straight to your inbox.

"*" indicates required fields

Or see our Guides, Calculators or Taxopedia